The Digital Euro Pilot: High Urgency for PSPs in 2026

- keyFinance Team

- 7 days ago

- 3 min read

The clock is ticking for Europe’s financial institutions. On May 14, 2026, at 17:00 CEST, the window for Payment Service Providers (PSPs) to join the European Central Bank’s official Digital Euro pilot officially slams shut. This is not merely a technical trial; it is a high-stakes entry point into the future of the Eurozone’s monetary sovereignty.

For leaders at keyFinanceInfo.com, this deadline represents the final opportunity to move from passive observation to active participation in the infrastructure that will likely anchor our retail economy by 2029.

As the ECB prepares to evaluate applicants by late June, the industry is bracing for a shift that promises to marry the digital convenience of card payments with the absolute privacy and finality of physical cash.

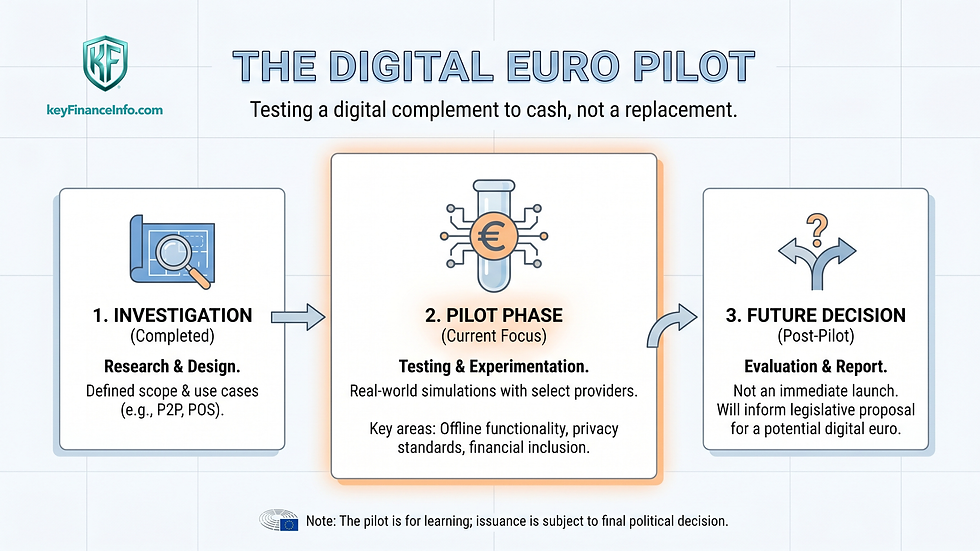

The Deadline and the Roadmap

The ECB’s call for expression of interest, launched in March, reaches its crescendo this week. PSPs who miss this 17:00 CEST deadline will be locked out of the primary development phase starting in July 2026.

Selection Outcome | Successful applicants will be notified by the end of June 2026. |

Operational Phase | While the "Technical Readiness" phase begins now, the actual live transactions within the pilot are scheduled for a 12-month window starting in mid-2027. |

Goal of the Pilot | Validating "use cases" like person-to-person (P2P) transfers, e-commerce, and physical point-of-sale (POS) interactions using the draft Digital Euro Scheme Rulebook. |

The Intraday Liquidity Revolution

For corporate treasurers, the IPR and the upcoming Digital Euro have turned cash flow forecasting into a high-frequency discipline. In the old world of batch processing, treasurers could predict their "end-of-day" position with relative ease. In May 2026, liquidity is a 24/7/365 moving target.

Companies are now forced to maintain higher "pre-funded" buffers in their settlement accounts to ensure that automated 10-second payments don't fail at 3:00 AM on a Sunday.

This shift is driving a surge in AI-driven liquidity steering tools that can predict payment outflows and optimize interest-bearing balances in real-time, effectively turning the "compliance burden" of IPR into a tool for razor-sharp working capital management.

Why the 2026 Framework is Different

Unlike previous digital payment innovations, the 2026 legislative framework under the Irish EU Presidency is doubling down on Privacy and Offline Capabilities.

Cash-Like Privacy | The 2026 pilot specifically tests "Offline Mode," where payments can be settled via Bluetooth or NFC without an internet connection. |

Holding Limits | To prevent a "bank run" into digital central bank money, the ECB is testing a tiered holding limit, likely capped at €3,000 per individual. |

Zero Cost for Consumers | A core pillar of the Regulation is that basic Digital Euro services must be free of charge for citizens, mirroring the experience of using physical coins and notes. |

From Transactional to Agentic Sanctions Screening

The 10-second execution limit has made traditional "stop-and-review" sanctions screening obsolete. To remain compliant without slowing down the economy, European banks have pivoted to Agentic Sanctions Auditing. Instead of checking every individual €50 payment against a list in real-time—which frequently caused timeouts and compliance failures—systems now use "Continuous Customer Screening."

AI agents maintain a live, verified "Green List" of pre-vetted entities, allowing transactions to fly through the 10-second window while the AI focuses its heavy processing power on high-risk, real-time anomalies. This is the new standard: screening the entity, not just the wire.

Frequently Asked Questions (FAQ) about The Digital Euro Pilot in 2026

What happens if a PSP misses the May 14th deadline?

No new applications or amendments will be accepted after the cutoff; these firms will have to wait for the general rollout, missing the chance to influence the technical standards.

Is the Digital Euro replacing physical cash?

No, the 2026 legislation mandates that it will coexist with and complement physical banknotes.

Will the Digital Euro be "programmable"?

The ECB has stated it will not be "programmable money" (e.g., money that expires), but it will support "conditional payments" like automated refunds or pay-on-delivery.

How does this impact card scheme fees?

By creating a domestic European infrastructure, the Digital Euro aims to reduce dependence on international card schemes, potentially lowering costs for merchants.

Can businesses hold Digital Euro?

Currently, the framework focuses on individuals; businesses can receive it but must generally "waterfall" the balance into their standard commercial bank accounts.

The Digital Euro Pilot in 2026

Comments